This website uses cookies so that we can provide you with the best user experience possible. Cookie information is stored in your browser and performs functions such as recognising you when you return to our website and helping our team to understand which sections of the website you find most interesting and useful.

Cryptocurrencies Issued by Central Banks – Anonymity, Inflation, Stability

Central Banks worldwide are testing digital currencies with the aim to follow the trends in digitization, exploiting the new technologies. The intent is to come closer to public demand for changes, which is a demand for faster, seamless and cheaper money flow, power over assets, etc. While the public is trying and pressuring, the governments are trying to keep the power over peoples’ money, especially after the announcement of the Facebook’s endeavors for creating a corporate cryptocurrency, called Libra Coin, a.k.a. the Facebook Money (you can read more about the Libra in our previous article).

In this article, we are going to discuss the latest report of the European Central Bank – Exploring anonymity in central bank digital currencies (hereinafter: “the report”) addressing the challenges that the digitization is bringing into banking and payment systems. According to the European Central Bank (hereinafter: ECB) embracing those challenges and welcoming the new technologies requires a balance between keeping (allowing) a certain degree of privacy in electronic payments yet also ensuring full compliance with regulations, which aim to tackle money laundering and the financing of terrorism (AML/CFT regulations).

In order to achieve that, the ECB has established a “proof of concept” which can be applied by central banks when issuing digital currencies (also known as Central Bank Digital Currencies or CBDCs – more about these in our previous article).

The report provides that “The proof of concept drawn up by the ESCB (European System of Central Banks, o.p.) demonstrates that it is possible to construct a simplified CBDC payment system that allows users some degree of privacy for lower-value transactions, while still ensuring that higher-value transactions are subject to mandatory AML/CFT checks.“

Features of CBDCs under to the Proof-of-Concept

Under the current proof-of-concept (hereinafter: the PoC), the CBDCs shall “provide for a digitized solution, built on DLT (distributed ledger technology) allowing a certain level of privacy, while ensuring the compliance with the AML/CTF Rules.”

Under the PoC, the CBDCs have the following features:

- CBDCs are treated the same as cash (have cash-like features),

- the emphasis is on users’ privacy for lower-value transactions,

- CBDCs shall be distributed to users by intermediaries, rather than a central bank – intermediaries shall be responsible for distributing CBDCs and offering custody,

- the central bank has a sole discretion to issue a CBDCs or remove them from circulation,

- The large volume transactions shall be checked and supervised by a dedicated AML authority,

- There will be a maximum wallet cap (limit) on CBDC holdings for individual users.

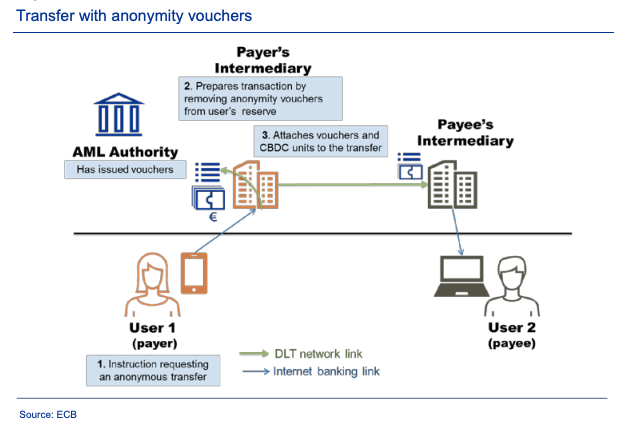

How the flow is designed can be seen in the picture below.

Privacy and Anonymity of Transactions

According to the report, each user shall be on-boarded by an intermediary (a bank or similar financial institution), which shall provide clients with pseudonymous identities that are used as network addresses for CBDC payments.

Users of the CBDC shall be allowed to transfer the digital currency anonymously up to a certain amount and within a certain timeframe, and the user’s transaction history shall be seen only to those institutions that a user chooses. It shall not be seen to the central bank and intermediaries by default.

The anonymity shall be limited to low volume transactions, which is the amount that a user can spend without the AML authority seeing transaction data. The concept is new and sets up so-called “Anonymity Vouchers”. The vouchers will be issued by the AML/CTF authority to users. If users will wish to transfer the CBDC anonymously, they will have to use the voucher(s). One CBDC unit transferred anonymously shall be exchanged for one Anonymity Voucher (1:1 exchange ratio).

Vouchers function as a tool for “calculating” the volume of anonymously transferred CBDCs up to the point of reaching the threshold. The vouchers will be obtainable for free and will not be transferable to another person.

What will be the volume limit (threshold) for anonymous transactions, it remains to be seen, but it will probably correspond to limits set in the AML Directive and FATF Guidelines.

Issuance, Limitation, and Removal of CBDC Units

According to the report, only the central bank will be allowed to issue and remove units of the CBDC from circulation.

By request of a user, an intermediary will open a request order at the central bank, on behalf of its user, and the central bank will issue the requested amount of CBDC units. The report also says that the issuing central bank shall not limit the supply of CBDC in a way that could lead to excess demand from its users.

However, limits will be applied at the level of each individual wallet. Conversion to and from CBDC shall always occur at a ratio of 1:1 in order to ensure that CBDC has the same value as alternative forms of the same currency, which is a similar approach as it is with commercial bank money, electronic money, and physical cash. The intermediary shall then add the CBDC units to the users’ accounts and his account with the private money, which is held by that same intermediary, shall be debited by that same (purchase) amount.

In simple words, intermediaries (commercial banks) will function as brokers for buying and selling CBDC units, which they will obtain from the central bank. There is a good chance that the intermediaries will charge a fee for the operation of the transactions.

In addition, users’ accounts will be subject to AML/CTF rules and KYC (client identification) onboarding process, whereas a certain amount of transactions will have the option to be privately transferred. It is the same logic as the one behind using cash when you have it in your pocket, only that this time the central authority will guarantee you that anonymity by giving you vouchers. The real anonymity here is debatable. One has to realize that if the CBDCs are going to live, there won’t be much anonymity for its users.

The transactions above the certain volume threshold shall be checked also, and the information about the transaction, sender, and recipient will have to be disclosed.

As it seems, this is not only a proof-of-concept for the CBDCs and intermediaries, but could be applied for the transactions carried out on current crypto exchanges offering brokerage or trading service for all kinds of (trading) pairs. The report does not say if the CBDC units will be obtainable (purchased or sold) on any of private cryptocurrency exchanges, which entities will be legitimate intermediaries and if the CBDCs are going to be traded on open exchanges for speculative purposes. It also doesn’t say how the CBDC system shall be integrated into retail, international trade, real estate transactions and all the other aspects of business and life.

Transactions

A payer will send a CBDC by sending a transfer instruction indicating the amount, the pseudonym of the payee and whether or not the payment should be made anonymously (using the voucher). The intermediary’s node will then initiate the transfer by following a process. This will be different for anonymous (low volume) transactions and transactions that need the involvement of the AML authority. In a case where the AML check will be mandatory, the mechanism will allow for intermediaries to perform AML checks. The transaction will be accepted by the payee’s intermediary with no need for approval from the AML authority if the payer used Anonymity Vouchers he has at his disposal.

The transaction flow is pictured below.

Intermediaries will be obliged to reject all anonymous transactions that:

- exceed the threshold,

- exceed a prescribed period of time,

- exceed the maximum cap of CBDC holdings.

The report states that “limiting the amount of CBDC at the level of individual wallets would indirectly allow the overall CBDC volume to be controlled if for example the number of wallets per citizen and the usage by non-citizens was restricted”.

Users will be able to exchange the CBDC units back to other currencies by opening a request with an intermediary. An intermediary will open a request at the central bank for the desired amount of the desired currency in exchange for the units of CBDC.

Open Questions

The European regulator is making great efforts towards embracing the blockchain/DLT technology, by bringing cryptocurrencies and payment systems closer together.

On the other hand, the main point (and the real value) of cryptocurrencies is decentralization, peer-to-peer transacting, making money flow faster and cheaper. It has the purpose of giving back people power over their money.

According to the discussed PoC, the concept is moving away from the purpose for which Bitcoin was created. The system in the report raises several questions about the monetary policy of the CBDC, namely:

– would CBDC be just an alternative for fiat money, physical cash, electronic money, or all of the mentioned?

– can there be more CBDC units than fiat money in circulation, and what can be the consequences of this?

– what will be CBDC backed by, and what will determine the utility (if any), purpose and, last but not least, the price?

– how will the stability of the CBDC be achieved?

– will CBDC be subject to inflation of fiat money and subject of its own inflation?

– what will attract demand for the CBDC units?

– would CBDC affect the interest rates?

– could CBDC trigger inflation of fiat money?

– could CBDC undermine financial stability and trigger financial crisis?

Our own considerations

There can be several benefits of applying CBDCs if applied carefully and with the best public interest in mind, such as safety of payment systems, seignorage income preservation, monetary inclusion, efficiency, seamless and cheaper transactions, competition in the banking sector, monetary safety, and more.

Notwithstanding the above, here are but a few of our own observations, made on the basis of the knowledge that we have and on the basis of the report we are discussing.

- Intermediaries. There are still going to be institutions (intermediaries), which will be charging fees. There is a good chance that requests and orders to be completed will depend on the business hours of institutions. The transaction will be centralized, ran through intermediaries, meaning not faster nor cheaper.

- Relative Anonymity. The transactions will not be pee-to-peer but will have to be checked beforehand. Even with using Anonymity Voucher, there will always be an authority that will have power over those vouchers, will issue and assign them, and will always have the knowledge about which user used them and how many. In case the “anonymity vail” needed to be pierced, the information about the user and transaction will be obtainable.

- Limitation of the number of wallets and CBDC units per individual. There is a good chance that the number of wallets per individual and the use of CBDC for non-citizen could also be restricted. The report reasons this with a claim that this would indirectly help the central banks to control the overall CBDC volume, however, there is no further explanation for that statement.

- Price, unlimited supply and inflation. CBDCs will be subject to unlimited creation and therefore inflation. There is also a consideration regarding the price of a CBDC unit and about the (unlimited) amount of CBDCs in circulation. Bitcoin (and most of the other cryptocurrencies) have a source code that outlines the finite supply and the maximum number of units ever to exist. Over time, it becomes more difficult to produce (mine) Bitcoins, up until the point where the upper limit is reached. Such a finite supply makes Bitcoin inherently deflationary and more akin to gold than fiat currencies. If the CBDC conversion ratio with the Euro is 1:1, this means that 1 CBDC unit is going to be issued and sold for 1 Euro. If the value of Euro drops, the CBDC price will follow, and vice versa. Moreover, taking into account the unlimited amount of CBDC units that can be issued by a central bank, there is a question of double inflation – the CBDC price will potentially drop not only with the inflation of the Euro but also with every new issuance of CBDC units. In addition to that, a question arises what happens if there are more CBDC units issues than there is a supply of fiat money available.

- Backing behind CBCD. The report does not address the question of backing the CBDC, however, we assume that the CBDCs will have to have it. As it looks now, the CBDC will be a creation of a new commodity, a new medium of exchange or means of payment, having no intrinsic value except the government’s claim it is worth something (such as most of the current fiat money systems) and a belief and trust in the new system.

It has to be emphasized, that such currency will not hold the benefits of Bitcoin (decentralization, anonymity and privacy, trust, deflationary nature, peer-to-peer technology, improvement of cross-border payments and enabling faster and cheaper transactions), but it is also questionable what (if any) reserves will CBDCs have.

If a CBDC, issued under this PoC, would be issued in Venezuela in 2018, the CBDC would not even have the nature of a stable coin, considering the hyperinflation in the past few years. - Jurisdiction. There is a question of using such CBDCs in different jurisdictions. A jurisdiction-specific wholesale CBDC which cannot be exchanged across borders offers little benefit over the existing model.

Conclusion

CBDCs, as described in the report, could potentially be a subject of instability, inflation, and high fees. Such a model can bring a lack of trust in the CBDCs for not having any intrinsic value or utility or for not having any reserve or guarantee behind, but being merely a parallel alternative for the current fiat money system.

CBDCs represent a great opportunity when designed and applied properly. We are looking forward to seeing the development of the concept and real-life implications.

IURICORN is here to help you with any questions regarding the CBDCs, you can reach us here.